Content previously posted on Keeping Current Matters

* This article was originally published here

Selling your house is no simple task. And when you sell on your own – known as a FSBO (or For Sale by Owner) – you’re responsible for handling some of the more difficult aspects of the process without the expert guidance you need.

The 2021 Profile of Home Buyers and Sellers from the National Association of Realtors (NAR) surveys homeowners who recently sold their house on their own and asks what difficulties they faced. Those sellers say some of the biggest headaches are prepping their house for sale, pricing it right, and handling the required paperwork.

Working with an agent is the best way to ensure you have an expert on your side to guide you at every turn. Agents have the skills and knowledge that are essential to navigating each step with ease, efficiency, and accuracy. Here are just a few things a real estate agent will do to make sure you get the most out of your sale.

Selling your house requires a significant amount of time and effort. Doing it right takes expertise and an understanding of today’s buyers. Your agent knows the answers to common questions, such as:

Your time and money are important, and you don’t want to waste either one focusing on the wrong things. A real estate advisor relies on their experience to answer these questions and more, allowing you to make the right investments to prep your house before you list.

Today, the average home is getting 3.6 offers per sale according to recent data from NAR. That’s great news if you’re planning to sell, since the more offers you receive, the more likely you are to sell your house in a bidding war, and for a higher price.

Real estate agents have an assortment of tools at their disposal, like social media followers and agency resources, that will ensure your house is viewed by the most buyers. Without access to these tools and your agent’s marketing expertise, your buyer pool – and your home’s selling potential – is limited.

Today, when a house is sold, more disclosures and regulations are mandatory, meaning the number of legal documents to juggle is growing. It’s hard to understand all the requirements and fine print (especially if you’re not an expert). That’s why your advisor is an invaluable guide.

Your agent knows exactly what needs to happen, what all the paperwork means, and can work through it efficiently. They’ll help you review the documentation and avoid any costly missteps that could happen if you tackle it on your own.

If you sell without an agent, you’ll also be solely responsible for all negotiations. That means you have to coordinate with:

Instead of going toe-to-toe with all these parties alone, lean on an expert. Your agent relies on experience and training to make the right moves throughout the negotiation. They’ll know what levers to pull, how to address each individual concern, and when you may want to get a second opinion. When you sell your house yourself, you’ll need to be prepared to have these conversations on your own.

Real estate professionals have the expertise to price your house accurately and competitively. To do so, they compare your house to recently sold homes in your area and factor in the current condition of your house. These factors are key to making sure your house is priced to move quickly and get you the maximum return on your investment.

When you sell as a FSBO, you’re operating without this advantage. That could cost you in the long run if you price your house too high or too low.

There’s a lot that goes into selling your house, and it takes time, effort, and expertise to truly maximize your sale. Instead of tackling it alone, let’s connect to make sure you have an expert on your side.

Content previously posted on Keeping Current Matters

Once you’ve found your dream home and applied for a mortgage, there are some key things to keep in mind before you close. It’s exciting to start thinking about moving in and decorating your new place, but before you make any large purchases, move your money around, or make any major life changes, be sure to consult your lender – someone who’s qualified to explain how your financial decisions may impact your home loan.

Here’s a list of things you shouldn’t do after applying for a mortgage. They’re all important to know – or simply just good reminders – for the process.

Lenders need to source your money, and cash isn’t easily traceable. Before you deposit any amount of cash into your accounts, discuss the proper way to document your transactions with your loan officer.

New debt comes with new monthly obligations. New obligations create new qualifications. People with new debt have higher debt-to-income ratios. Since higher ratios make for riskier loans, qualified borrowers may end up no longer qualifying for their mortgage.

When you co-sign, you’re obligated. With that obligation comes higher debt-to-income ratios as well. Even if you promise you won’t be the one making the payments, your lender will have to count the payments against you.

Remember, lenders need to source and track your assets. That task is much easier when there’s consistency among your accounts. Before you transfer any money, speak with your loan officer.

It doesn’t matter whether it’s a new credit card or a new car. When you have your credit report run by organizations in multiple financial channels (mortgage, credit card, auto, etc.), your FICO® score will be impacted. Lower credit scores can determine your interest rate and possibly even your eligibility for approval.

Many buyers believe having less available credit makes them less risky and more likely to be approved. This isn’t true. A major component of your score is your length and depth of credit history (as opposed to just your payment history) and your total usage of credit as a percentage of available credit. Closing accounts has a negative impact on both of those determinants of your score.

Any blip in income, assets, or credit should be reviewed and executed in a way that ensures your home loan can still be approved. If your job or employment status has changed recently, share that with your lender as well. The best plan is to fully disclose and discuss your intentions with your loan officer before you do anything financial in nature.

Content previously posted on Keeping Current Matters

It’s clear that owning a home makes financial sense. But lately, the emotional side of what drives homeownership is becoming increasingly important.

No matter the living space, the feeling of a home means different things to different people. Whether it’s a familiar scent or a favorite chair, the feel-good connections to our own homes can be more important to us than the financial ones. Here are some of the reasons why.

You’ve put in a lot of work to achieve the dream of homeownership, and whether it’s your first home or your fifth, congratulations are in order for this milestone. You’ve earned it.

Owning your own home offers not only safety and security but also a comfortable place where you can simply relax and unwind after a long day. Sometimes that’s just what we need to feel recharged and truly content.

Whether you want more room for your changing lifestyle (think: working from home, dedicated space for a hobby, or a personal gym) or you simply prefer to have a large backyard for entertaining, you can invest in a home that truly works for your evolving needs.

Looking to try one of those decorative wall treatments you saw on Pinterest? Tired of paying an additional pet deposit for your apartment building? Maybe you want to create an entire in-home yoga studio. You can do all of these things in your own home.

Whether you’re a first-time homebuyer or a repeat buyer who’s ready to start a new chapter in your life, now is a great time to reflect on the non-financial factors that turn a house into a happy home.

Content previously posted on Keeping Current Matters

To succeed as a buyer in today’s market, it’s important to understand which market trends will have the greatest impact on your home search. Danielle Hale, Chief Economist at realtor.com, says there are two factors every buyer should keep their eyes on:

“Going forward, the conditions buyers face are primarily dependent on two things: mortgage rates and housing supply.”

Here’s a look at each one.

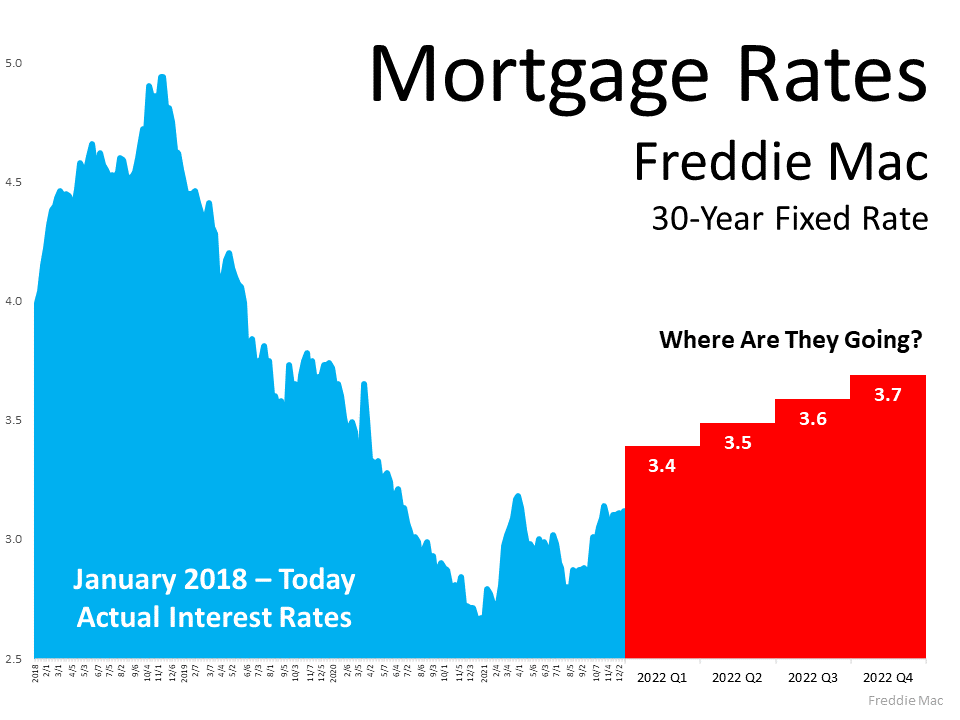

As a buyer, your interest rate directly impacts how much you’ll pay on your monthly mortgage when you purchase a home. Rates are beginning to rise, and experts forecast they’ll continue going up in 2022 (see graph below): As the graph shows, mortgage rates are expected to climb next year. But they’re still low when you compare to where they were just a few years ago. That presents today’s buyers with some motivation to lock in a low mortgage rate before they climb higher.

As the graph shows, mortgage rates are expected to climb next year. But they’re still low when you compare to where they were just a few years ago. That presents today’s buyers with some motivation to lock in a low mortgage rate before they climb higher.

The other market condition buyers need to monitor is the number of homes available for sale today. The latest Existing Home Sales Report from the National Association of Realtors (NAR) shows the current supply of inventory sits at just 2.4-months. To put that into perspective, a 6-month supply is ideal for a balanced market where there are enough homes to meet buyer demand.

However, there may be good news for buyers who are waiting for more options. A recent realtor.com survey shows more sellers are planning to list their homes this winter, meaning more choices will likely be available soon.

Even if your options improve some this season, it won’t significantly shift market conditions overnight. According to NAR, many more listings need to be available to move closer to a more neutral market:

“Given the average monthly demand . . . , 3.55 million homes should be on the market to meet a level of inventory equal to six months of demand, implying a shortage of homes for sale of 2.24 million.”

So remember, even with more homes expected to come to market this season, competition among buyers will remain fierce as there still won’t be enough homes for sale to meet the current demand. That means you’ll need to act quickly when you’re ready to make an offer.

If you’re planning on buying a home this winter, more options are welcome news, but it doesn’t mean you should slow down. Let’s connect today so you have an expert on your side to help act as quickly as possible when the right home for you hits the market.

Content previously posted on Keeping Current Matters

I first shared the story about this Christmas tree a few

years ago. One

of those situations where a senior passed and there were some

things that no one wanted. Little did I know what history would unfold.

As best as I can determine, the tree is 63 years old this

year. It has no great monetary value. It does have a lifetime and history of

hopefully happy times with family and social gatherings – none of which we will

ever know. Perhaps history is best seen through the sparkle still within this

tree and the spirit of Christmas wherever its destiny may lead it next.

In my 2019 post https://www.sanantoniorealestate.blog/2019/12/a-christmas-tree-story.html , I mentioned that the original carton had a date stamp that appeared to be either 1953 or 1958. The condition of the carton and disintegration of the carboard made that a challenge. So, this year, I took it a little further and checked the patents. Based on a patent filing approved in 1959, and some historical research about the company, 1958 can best be assumed the correct year. I learned something about patents too as it was not unusual to go into production while the patent was being registered.

Most of what follows in a repost of what was in my 2019

article about this tree….

The tree was manufactured in

Wisconsin by the Evergleam Company. There is a great article about Evergleam

written by Dave Hoekstra (1) and another by the Manitowoc County Historical Society

(2). It goes back to a time when manufacturing in America was the norm and

aluminum Christmas trees have a history of their own in that era – more can be

found in Wikipedia (3). Aluminum trees were “the rage” for quite a while in

homes across America and the American spirit of competitiveness kicked in

creating a market for trees having under 100 branches to those with over 400

branches and everything in between depending on the height of the tree. There

was an appliance - furniture retailer in Chicagoland known as Polk Brothers

(now gone) and it’s leader, Sol Polk known for his marketing savvy who

popularized aluminum trees and plastic Santa’s that were about 5 feet tall (4)–

by making either available for $5 with a purchase!

Aluminum tree popularity continued,

and folks tried hard to make theirs “different”. The trees came with a warning

not to use string lights that were so popular on “live” trees – and some folks

were “shocked” to find out that was good advice!

The lighting of the day was

typically a flood light. The flood light was either white, a static color or

even more popular was a rotating wheel that caused the tree to change color in

a slow continuous cycle. Today, I create that effect with a low energy led.

And then there was the pink aluminum

Christmas tree – check an article by WUWM (5) from Milwaukee. You can buy

aluminum trees today on eBay (6) and Esty (7).

The tree is still not for sale! But the challenge is on to

find a new home and someone who will care for it for at least the next 37 years

and share the story on its 100th birthday!

Hope y’all have a very Merry Christmas – just about a week

to go!

None of the links below are monetized. If you want to read more, these are a start. If you are curious and research leads you to discover any other cool information, please share it with me.

http://www.davehoekstra.com/2018/12/05/imy-first-evergleam-christmas-tree/

https://www.manitowoccountyhistory.org/programs/aluminumtrees

https://en.wikipedia.org/wiki/Aluminum_Christmas_tree

https://www.ebay.com/b/Aluminium-Christmas-Tree/33849/bn_55186952?rt=nc&_pgn=5

https://www.etsy.com/market/evergleam

And, since I never ever want to do the patent research again, sharing screen captures from that...

![2022 Housing Market Forecast [INFOGRAPHIC] | Simplifying The Market](https://files.simplifyingthemarket.com/wp-content/uploads/2021/12/15133912/20211217-KCM-Share-549x300.png)

![2022 Housing Market Forecast [INFOGRAPHIC] | Simplifying The Market](https://files.simplifyingthemarket.com/wp-content/uploads/2021/12/15133751/20211217-MEM.png)

Black Friday and Cyber Monday are over, which means some shoppers have wrapped up their holiday buying. But there’s still a group of buyers that are very active this holiday season – homebuyers.

Experts anticipate the real estate market will see a flurry of activity this winter, and that’s great news for today’s sellers. If you’re planning on listing your home, there’s no need to wait until the spring for better conditions – today’s real estate market is already heating up.

The past 18 months brought about significant lifestyle changes for many of us, including the rise in remote work, job changes, and even early retirement for some. For many people, it’s prompting a search for their next home now rather than waiting for warmer months.

Lawrence Yun, Chief Economist at the National Association of Realtors (NAR), points out how this winter may see a significant number of sales:

“Compared to other past winter seasons, this winter season’s sales activity will be stronger. . . . This winter, there will be more sales compared to pre-pandemic winters going back all the way to 2006.”

You might be wondering: what does strong sales activity mean for you? It means there are likely to be more buyers active in the market this winter – far more than more normal, pre-pandemic years.

In the same article, Danielle Hale, Chief Economist for realtor.com, puts it in these simple terms:

“Sellers can expect to see plenty of buyers.”

The more buyers there are in the market, the more likely it is your home will get noticed. That can lead to a multiple-offer scenario or a potential bidding war. Receiving multiple offers on your home means you can select the right offer and terms for your situation – so you can truly win as a seller when you list your house this winter.

If you’re thinking about selling your house, you don’t need to wait until the spring. Buyers are ready now. Let’s connect to discuss why selling this holiday season could be the gift that keeps on giving.

Content previously posted on Keeping Current Matters

The sense of pride you’ll feel when you purchase a home can’t be overstated. For first-generation homebuyers, that feeling of accomplishment is even greater. That’s because the pride of homeownership for first-generation buyers extends far beyond the homebuyer. AJ Barkley, Head of Neighborhood and Community Lending for Bank of America, says:

“Achieving this goal can create a sense of pride and accomplishment that resonates both for the buyer and those closest to them, including their parents and future generations.”

In other words, your dream of homeownership has far-reaching impacts. If you’re about to be the first person in your family to buy a home, let that motivate you throughout the process. As you begin your journey, here are three helpful tips to make that dream come true.

It’s important to reach out to a trusted advisor early in your homebuying process. Not only can an agent help you find the right home, but they’ll serve as your expert advisor and answer any questions you might have along the way.

The latest Profile of Home Buyers and Sellers from the National Association of Realtors (NAR) surveyed first-time homebuyers to see how their agent helped them with their home purchase (see chart below):

As the graph shows, your agent is a great source of information throughout the process. They’ll help you understand what’s happening, assess a home’s condition, and negotiate a contract that has the best possible terms for you. These are just some of the reasons having an expert in your corner is critical as you navigate one of the most significant purchases of your life.

The second piece of advice for first-generation homebuyers is practical: do your research so you know what you can afford. That means getting your finances in order, reviewing your budget, and getting pre-approved through a lender. It also means learning the ins and outs of what it takes to pay for your home, including what you’ll need for a down payment.

Many homebuyers believe the common misconception that you can’t purchase a home without coming up with a 20% for a down payment. As Freddie Mac says:

“The most damaging down payment myth—since it stops the homebuying process before it can start—is the belief that 20% is necessary.”

The chart below shows what recent homebuyers have actually put down on their purchases:

On average, first-time buyers only put 7% down on their home purchase. That’s far less than the 20% many people believe is necessary. That means your down payment, and your home purchase, may be in closer reach than you realize. Keep that in mind as you work with a real estate professional to better understand what you’ll need for your purchase.

Finally, it’s important keep in mind why you’re searching for a home to begin with. Overwhelmingly, first-generation homeowners recognize the financial and non-financial benefits of owning a home. In fact, in a recent survey:

As AJ Barkley explains:

“For many first-generation homeowners and their families, homeownership has a unique importance, given the collective efforts to overcome financial challenges that can often span generations…”

If you’re a first-generation homebuyer, being prepared and working with a trusted expert is key to achieving your dream. Let’s connect today so you can get started on your path to homeownership.

Content previously posted on Keeping Current Matters

From the opportunity to take advantage of today’s low mortgage rates to changing homeowner needs, Americans have more motivation than ever to buy a home. According to the experts, buyers are making moves right now, creating an unseasonably strong housing market for this time of year.

As we wrap up the fall season and move into the winter months, here’s a look at what several industry leaders have to say about the continued momentum in the current market, and what it means as we head into the early part of next year.

“This solid buying is a testament to demand still being relatively high, as it is occurring during a time when inventory is still markedly low. The notable gain in October assures that total existing-home sales in 2021 will exceed 6 million, which will shape up to be the best performance in 15 years.”

“So far in November, purchase applications point to another strong month in sales. Still low rates and demographic demand support this strength, even as affordability and inventory headwinds remain.”

“The demand for housing in the United States has reached a fever pitch, a trend that opposes the norm of this time of the year when the market cools as the winter months set in.”

“Strong demographic demand will continue to act as the wind in the housing market’s sails.”

Buyers are actively in the market, and they’re competing for homes to purchase. With the momentum coming out of this fall, all signs point to the winter housing market picking up steam, making it much busier than in a more typical year. And as we’ve seen in so many ways, 2020 and 2021 were anything but typical in real estate. It looks like 2022 may be joining that list before we know it.

If you think the housing market will slow down this winter, think again. Whether you’re thinking of buying a home, selling your house, or both – let’s connect to determine if this winter is your best time to make a move too.

Content previously posted on Keeping Current Matters![A Happy Tail: Pets and the Homebuying Process [INFOGRAPHIC] | Simplifying The Market](https://files.simplifyingthemarket.com/wp-content/uploads/2021/12/08135234/20211210-KCM-Share-549x300.png)

![A Happy Tail: Pets and the Homebuying Process [INFOGRAPHIC] | Simplifying The Market](https://files.simplifyingthemarket.com/wp-content/uploads/2021/12/08135237/20211210-MEM.png)

If you’re a homeowner who’s decided your current house no longer fits your needs, or a renter with a strong desire to become a homeowner, you may be hoping that waiting until next year could mean better market conditions to purchase a home.

To determine whether you should buy now or wait another year, you can ask yourself two simple questions:

Let’s shed some light on the answers to both of these questions.

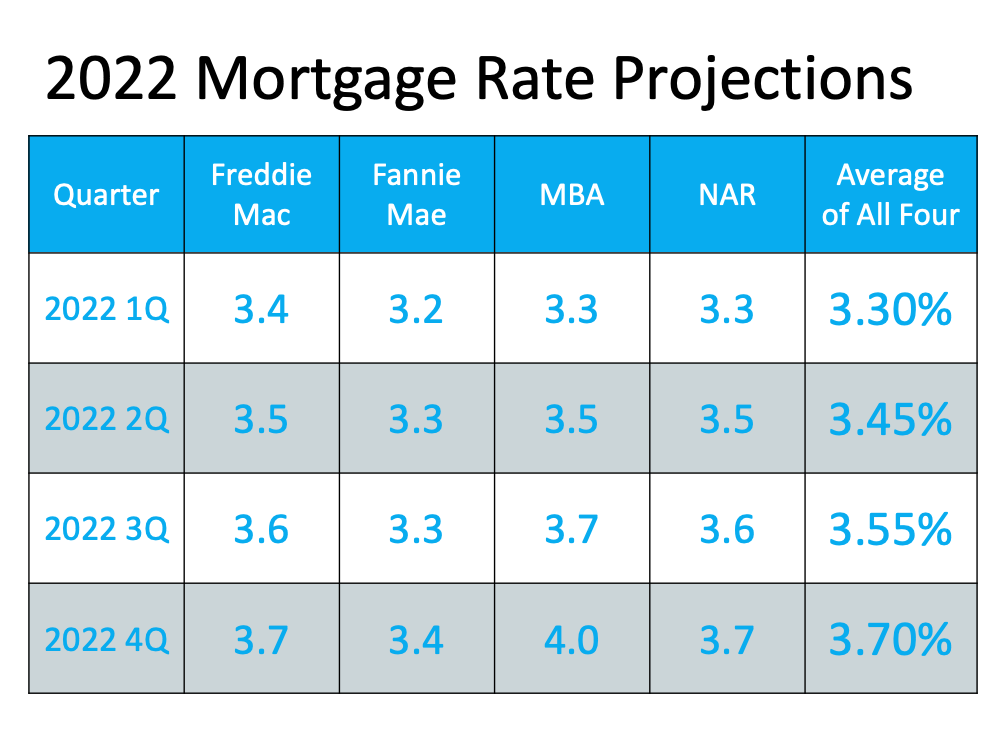

Three major housing industry entities are projecting ongoing home price appreciation in 2022. Here are their forecasts:

According to the National Association of Realtors (NAR), the median price of a home today is $353,900. Using an average of the three price projections above (6.53%), a home that sold for $353,900 today would be valued at $377,010 at the end of next year. As a prospective buyer, you would therefore pay an additional $23,110 by waiting.

Today, Freddie Mac estimates the average 30-year fixed mortgage rate in the fourth quarter of this year will be 2.8%. However, most experts believe mortgage rates will rise as the economy recovers. Here are the forecasts for the fourth quarter of 2022 by the three major entities mentioned above:

That averages out to 3.73% if you include all three forecasts. Any increase in mortgage rates will increase your costs.

If both variables increase, you’ll pay a lot more in mortgage payments each month. Let’s assume you purchase a $353,900 home in the fourth quarter of this year with a 30-year fixed-rate loan at 2.8% after making a 10% down payment. According to mortgagecalculator.net, your monthly mortgage payment would be approximately $1,309 (this does not include insurance, taxes, and other fees because those vary by location).

That same home one year from now could cost $377,010, and the mortgage rate could be 3.73% (based on the industry forecasts mentioned above). Your monthly mortgage payment after putting down 10%, would be approximately $1,568. The difference in your monthly mortgage payment would be $259. That’s $3,108 more per year and $93,240 over the life of the loan.

The difference in your monthly mortgage payment would be $259. That’s $3,108 more per year and $93,240 over the life of the loan.

Add to that the approximately $23,110 a house with a similar value would build in home equity this year due to home price appreciation, and the total net worth increase you could gain by buying this year is over $115,000 (the $93,240 mortgage savings plus the $23,110 potential gain in equity if you buy now).

When asking if you should buy a home, you may think of the non-financial benefits of homeownership. When asking when to buy, the financial benefits make it clear that doing so now is much more advantageous than waiting until next year.

Content previously posted on Keeping Current Matters

There’s no question that the financial benefits of selling a house are outstanding today. Now is truly a great time to list if you’re ready to make a change. But if you do sell your house right now, you may be wondering where you’ll go when you move.

With so few homes available to buy right now, you might be considering building a new home as one of your options. But you may be unsure if that’s the way to go. Let’s compare the benefits of a newly built home versus moving into an existing one, and why working with a real estate agent throughout the process is mission-critical to your success no matter what you decide.

First, let’s look at the benefits of purchasing a newly constructed home. With a brand-new home, you’ll be able to:

If you build a home from the ground up, you’ll have the option to select the custom features you want, including appliances, finishes, landscaping, layout, and more.

When building a home, you can choose energy-efficient options to help lower your utility costs, protect the environment, and reduce your carbon footprint.

Many builders offer a warranty, so you’ll have peace of mind on unlikely repairs. Plus, you won’t have as many little projects to tackle. QuickenLoans puts it like this:

“Buying a new construction vs. existing home typically means you’ll have fewer repairs to do. It can be a huge relief to know that it’s unlikely you’ll have to repair the roof or replace the furnace.”

Another perk of a new home is that nothing in the house is used. It’s all brand new and uniquely yours from day one.

Now, let’s compare that to the perks that come with buying an existing home. With a pre-existing home, you can:

With decades of homes to choose from, you’ll have a broader range of floorplans and designs available.

Existing homes give you the option to get to know the neighborhood, community, or traffic patterns before you commit.

Established neighborhoods also have more developed landscaping and trees, which can give you additional privacy and curb appeal. As Investopedia says, if you buy an existing home:

“Odds are, too, that the home will have mature landscaping, so you won’t have to worry about starting a lawn, planting shrubs, and waiting for trees to grow.”

The character of older homes is hard to reproduce. If you value timeless craftsmanship or design elements, you may prefer an existing home. According to Houseopedia:

“Charm is priceless. Existing homes, especially those built in the 1950’s or before, often offer architectural elements, historic charm and a quality of craftsmanship not available in new homes.”

The choice is yours. When you start your search for the perfect home, remember that you can go either route – you just need to decide which features and benefits are most important to you. Working with the guidance of your trusted real estate advisor will help you make the most informed and educated decision, so you can move into the home of your dreams.

If you have questions about the options in your area, let’s discuss what’s available and what’s right for you, so you’re ready to make your next move with confidence.

Content previously posted on Keeping Current Matters

Since the pandemic began, Americans have reevaluated the meaning of the word home. That’s led some renters to realize the many benefits of homeownership, including the feelings of security and stability and the financial benefits that come with rising home equity. At the same time, many current homeowners have decided their house no longer meets their needs, so they moved into homes with more space inside and out, including a home office for remote work.

However, not every purchaser has been able to fulfill their desire for a new home. Here are two obstacles some homebuyers are facing:

This past week, both of those challenges have been mitigated to some degree for many purchasers. The FHFA (which handles mortgages by Freddie Mac, Fannie Mae, and the Federal Housing Administration) is raising its loan limit for prospective purchasers in 2022. The term used to describe the maximum loan amount they will entertain is the Conforming Loan Limit.

Investopedia explains the difference in a recent post:

“Conforming loans are the only loans that meet the requirements to be acquired by Fannie Mae and Freddie Mac. Jumbo loans, which exceed the conforming limit, are the most common type of nonconforming loan.”

A Forbes article earlier this year explains the benefits of a conforming loan and why they exist:

“Since lenders can’t sell non-conforming loans to Fannie Mae or Freddie Mac to free up their cash, they’re a bit riskier for the lender. This is especially true for jumbo loans, which aren’t backed by any government guarantees. If you default on a jumbo loan, it’s a huge blow to the lender.

Thus, lenders generally charge higher interest rates to compensate, and they can have even more requirements. For example, lenders who give out jumbo loans often require that you make a down payment of at least 20% and show that you have at least six months’ worth of cash in reserve, if not more.”

The FHFA has significantly increased its Conforming Loan Limits for 2022. Sandra L. Thompson, FHFA Acting Director, explains in the press release that:

“Compared to previous years, the 2022 Conforming Loan Limits represent a significant increase due to the historic house price appreciation over the last year. While 95 percent of U.S. counties will be subject to the new baseline limit of $647,200, approximately 100 counties will have conforming loan limits approaching $1 million.”

This means that more homes now qualify for a conforming loan with lower down payment requirements and easier lending standards – the two challenges holding many buyers back over the last year.

The Federal Housing Administration (FHA) also increased its Conforming Loan Limits for 2022. That could also mean an easier path to homeownership for many prospective buyers. As the Forbes article explains:

“FHA loans can be very beneficial if you don’t have as much savings, or if your credit score could use some work.”

Buying your first or your next home may have just gotten much easier (less stringent qualifying standards) and less expensive (possibly lower mortgage rate). Let’s connect to discuss how these changes may impact you.

If you’re trying to decide when to sell your house, there may not be a better time than this winter. Selling this season means you can take advantage of today’s strong sellers’ market when you make a move.

Right now, conditions are very favorable for current homeowners looking for a change. If you sell now, here’s what you can expect:

In addition to these great perks, you’ll also win big on your next move if you sell now. CoreLogic reports homeowners gained an average of $51,500 in equity over the past year. This wealth boost is the result of buyer competition driving home prices up. You can leverage that equity to fuel a move, before mortgage rates and home prices climb higher. To get a feel for how rates are projected to rise, see the chart below. The longer you wait to make your move, the more it will cost you down the road. As mortgage rates rise, even modestly, it will impact your monthly payment when you purchase your next home. Waiting just a few months to make that change could mean a long-term financial impact.

The longer you wait to make your move, the more it will cost you down the road. As mortgage rates rise, even modestly, it will impact your monthly payment when you purchase your next home. Waiting just a few months to make that change could mean a long-term financial impact.

The good news is today’s rates are still hovering in a historically low range. According to Doug Duncan, Senior VP and Chief Economist at Fannie Mae:

“Right now, we forecast mortgage rates to average 3.3 percent in 2022, which, though slightly higher than 2020 and 2021, by historical standards remains extremely low . . .”

Selling before rates climb higher means you can make your move and lock in a low rate on the mortgage for your next home. This helps you get more home for your money and keeps your payments down too.

As a homeowner, you have a great opportunity to get the best of both worlds this season. You can truly win when you sell and when you buy. If you’re thinking about making a move, let’s connect so you have the information you need to get the process started.

Content previously posted on Keeping Current Matters![A Checklist for Selling Your House This Winter [INFOGRAPHIC] | Simplifying The Market](https://files.simplifyingthemarket.com/wp-content/uploads/2021/12/01091740/20211203-KCM-Share-549x300.png)

![A Checklist for Selling Your House This Winter [INFOGRAPHIC] | Simplifying The Market](https://files.simplifyingthemarket.com/wp-content/uploads/2021/12/01091743/20211203-MEM.png)

If you’re living on your own and looking to buy a home, know that you can make your dream a reality with thoughtful planning and the right team of experts. Research from Freddie Mac shows 28% of all households (36.1 million) are sole-person, and that number is growing. Over the past 40 years, the number of sole-person households has nearly doubled, and that’s a trend that’s expected to continue. According to Freddie Mac:

“Our calculation suggests that there will be an additional 5 million sole-person households in the United States by the next decade. This means 42% of the household growth will be contributed by sole-person households, . . .”

If you fall into this category, here are three tips to help you achieve your homeownership goals.

When you buy a home on your own, you have to qualify for your loan based solely on your own finances and credit history. Investopedia says:

“. . . lenders will be looking at just one credit profile: yours. Needless to say, it has to be in great shape. It is always a good idea to review your credit report beforehand, and this is especially true of solo buyers.”

It’s important to find out your score so you know where it falls. If you’re not sure if it’s strong enough or where to focus your energy to improve it, meet with a professional for expert advice on your individual situation.

Next, look into down payment programs so you can get a feel for what you’ll need to save to buy a home. Rob Chrane, CEO of Down Payment Resource, explains:

“Buyers should discuss their program options with their loan officer and real estate agent to make sure they choose the program best suited to their personal needs.”

In this step, lean on the pros to determine what you’re eligible for and what’s right for you.

You should also spend time thinking about what you want. What type of home do you picture yourself in? To answer that question, Quicken Loans shares this advice:

“Think about your lifestyle, what you want out of your home and your needs. Is being close to work important? Do you need a lot of yard space? Do you want an extra bedroom that you can transform into a home office? Condo or detached home? Lots of space for entertaining? It’s all up to you (and your budget).”

Again, a professional can help you balance what you want and how much you should spend on your monthly housing costs to determine what type of home is right for you.

While buying a home solo can feel like a big challenge, it doesn’t have to be. If you lean on the professionals, they can help you navigate these waters and make sure you’re able to take advantage of the great opportunities in today’s housing market (like low mortgage rates) to buy your dream home.

The share of sole-person households is growing. If you’re looking to buy a home on your own, be confident that the dream is achievable. When you’re ready to begin your search, let’s connect so you have expert advice each step of the way.

Content previously posted on Keeping Current Matters

The game of chess can provide incredible lessons to apply to all aspects of life, including the homebuying process. Chess requires you to plan and think about your strategy from the very beginning of the game.

The homebuying process, like chess, requires strategy and planning. Here are a few things to keep in mind to ensure your plan is as strong as possible when you begin your home search.

It’s important to have a great opening play when you’re buying a home. And the best move you can make when you begin your home search is getting pre-approved by a lender. You’ve probably already heard this is an important step, but what exactly is pre-approval and what benefits does it provide you?

As Freddie Mac puts it:

“The pre-approval letter from your lender tells you the maximum amount you are qualified to borrow. Getting a pre-approval letter is not a loan guarantee, it simply states how much your lender is willing to lend you. . . .”

And while determining how much you can afford at the start of your search is critical, the pre-approval letter also serves another important purpose. Freddie Mac also notes:

“This pre-approval allows you to look for a home with greater confidence and demonstrates to the seller that you are a serious buyer.”

In the game of chess, a strong opening move signals to your opponent that you’re a serious competitor. As a homebuyer, your pre-approval letter signals to the seller that you’re a serious, interested buyer.

Every step you take to create your strategy as a buyer is important in today’s market. Why? Mortgage rates are still low, but increasing. Prices are going up. There’s a limited supply of homes for sale. These are just a few key variables in today’s market you need to be prepared for.

That means leaning on expert guidance as you plan every move is more important than ever. Have a team of professionals – like your trusted real estate agent and a loan officer – every step of the way to make sure you make the right moves.

Getting a pre-approval letter isn’t just good strategy, it can be game-changing. It allows you to get a full understanding of what you can afford, and it signals to sellers that you’re serious. Let’s connect today to ensure you’re playing chess and being strategic during the home buying process.

Content previously posted on Keeping Current Matters

There’s no denying the financial benefits of homeownership, but what’s often overlooked are the feelings of gratitude, security, pride, and comfort we get from owning a home. This year, those emotions are stronger than ever. We’ve lived through a time that has truly changed our needs and who we are, and as a result, homeownership has a whole new meaning for many of us.

According to the 2021 State of the American Homeowner report by Unison:

“Last year, staying home became a necessity and that caused many homeowners to have renewed gratitude for the roof over their head.”

As a nation, we continue to work through the challenges of a pandemic that’s pushed us all to new limits. Over the past year and a half, we’ve spent more time than ever at home: working, eating, schooling, exercising, and more. The world around us changed almost overnight, and our homes were redefined. Our needs shifted, and our shelters became a place that protected us on a whole new level. The same study from Unison notes:

It’s no surprise this study also reveals that homeowners are now more emotionally attached to their homes as well: As we’ve learned throughout this health crisis, homeownership can provide the safety and security we crave in a time of uncertainty. That sense of connection and emotional stability genuinely reaches beyond just the financial aspect of owning a home. As JD Esajian, President of CT Homes, LLC, says:

As we’ve learned throughout this health crisis, homeownership can provide the safety and security we crave in a time of uncertainty. That sense of connection and emotional stability genuinely reaches beyond just the financial aspect of owning a home. As JD Esajian, President of CT Homes, LLC, says:

“Aside from the financial factors, there are several social benefits of homeownership and stable housing to consider. It has long been thought that buying a home contributes to a sense of accomplishment. Still, most individuals fail to realize that homeownership can benefit your mental health and the community around you.”

Whether you’re thinking of buying your first home, moving up to your dream home, or downsizing to something that better fits your changing lifestyle, take a moment to reflect on what Mark Fleming, Chief Economist at First American, notes:

“Buying a home is not just a financial decision. It’s also a lifestyle decision.”

If you’re considering buying a home, it’s not entirely about the dollars and cents. Don’t forget to weigh the non-financial benefits that may truly change your life when you need them most.

Content previously posted on Keeping Current Matters