* * * THIS IS NOT AN ADVERTISEMENT * * *

If you are just viewing this article and have not yet read Part One, please go back two weeks to the first of the series; begin there followed by Part Two a week ago. I am sharing this with you as a public service - no monetary or other consideration is exchanged between Tim and myself. Find out more about how we know each other in Part One today! Al Cannistra

Our Guest Author today: Tim Allen, BA, MM, CSA

“What Kind of Medicare Plan Might Fit Your Unique Needs?” (part three)

Client Tales – Part Three of a Three-Part Series

Welcome to Part 3 of Client Tales, where we’ve been sharing stories about Medicare beneficiaries, what plans worked best for each one and why. With Annual Enrollment right around the corner, the goal of this series is for you to be able to know which of the various options out there might best fit your unique needs and to help you avoid costly mistakes. Any information we provide is limited to those plans we do offer in your area. Please contact Medicare.gov or 1-800-MEDICARE to get information on all your options.

So far in this series we have looked at Medicare Advantage HMO and PPO plans as well as Medigap supplement Plans G and High Deductible G through the eyes of my clients. We’ve shared stories based on my real-life clients to help bring the plans to life and to determine which plan might be better suited in a variety of life situations. I hope that you’ve seen through these true stories that there is no “one size fits all!”

In this session we will look at plans for people with chronic health conditions as well as for military veterans. We’ll also compare them side by side and end with a short quiz designed to help you determine what might be a good fit for you.

Below is a chart, which may be helpful to compare the costs of an HMO, PPO, or Medicare Advantage plan (in the 2nd Column) to the Plan G supplement and High Deductible G plans that we talked about in our first two podcasts.

The figures you see above are for a female, non-smoker, aged 65 based on current 2022 plan options. Notice that the premium of a Medicare Advantage Plan might be as low as $0, or it could be $25 for some PPO plans. They include Part D and most have no medical deductible. The annual premiums + the maximum out-of-pocket will be $0 if the plan is never used but could be as high as $12,500 with high utilization out of network.

You would pay $2,066.16 with a Plan G if you never use it; If fully utilized, your annual cost would be $2,299.16.

Now look at the High Deductible G. If never used, your maximum out-of-pocket would be $804.96. In a bad year where everything that could go wrong did go wrong your maximum out-of-pocket would be $3,294.96.

My wife and enrolled in and love this plan because we have the freedom to see any provider who accepts Medicare and risk of financial loss is reasonably low.

Medigap Supplement Plans C, Plan F and Plan F High Deductible are still available to people who turned 65 prior to January 1, 2020.

Plans C, F and F High Deductible may have a higher premium cost, but they have no separate Part B deductible. If you turned 65 prior to January 1st of 2020 and are interested in one of these plans, please click here to contact me or capture this QR code:

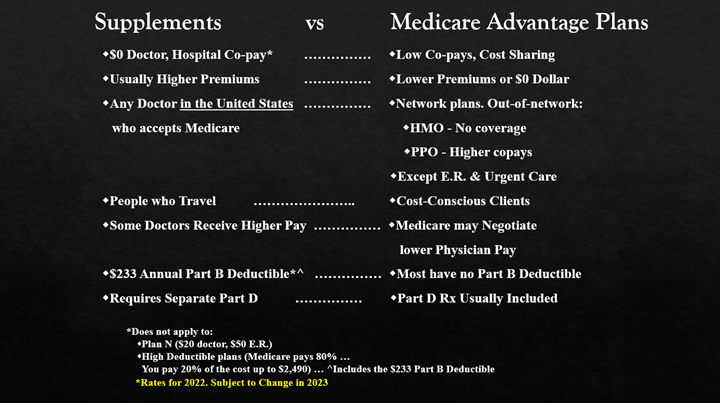

There is no one-size-fits-all! But when we compare Medicare supplements to Medicare Advantage plans, the light bulb clicks on in the minds of my clients and most become comfortable with what type of plan might fit their needs. For example, the chart below shows that:

• Except for a deductible, supplements will cost $0 Doctor & Hospital cost vs Low copays for Medic Advantage plans.• Usually, supplements have higher premiums vs lower or $0 premium.

• You may see any doctor who accepts Medicare in the United States on a supplement vs. no coverage out-of-network on an HMO, and higher cost out-of-network on a PPO. You can receive care in an emergency room anywhere in world on both plans and most but not all Urgent Care is considered in-network for both.• People who travel like the freedom of the supplement vs. cost-conscious clients who prefer low or no premiums.• There is a $233 annual Pt. B deductible vs. none on most Medicare Advantage plans.• Medigap supplements require a separate Pt. D plan but are included in most Medicare Advantage plans.

Most Medigap supplements do not offer value-added services vs. Medicare Advantage plans as in the chart below:

All plans offer worldwide E.R. But know this: The person who has only Medicare and no supplement or advantage plan does NOT have emergency or urgent care coverage worldwide. And remember, if you have only Medicare, you are only covered at 20%, which leaves you at risk for catastrophic financial loss.

If you know anyone who has a chronic illness such as diabetes, heart failure, chronic obstructive pulmonary disease (COPD), cardiovascular disease, or someone on kidney dialysis, Click here to contact me. We carry plans that are especially designed for them. There is a chronic illness form that they will need to fill out so and I’ll be happy to provide more information.

I reside and work in San Antonio, a great military city. If you are a veteran, kudos to you & a major shout out. Thank you for your service.

If you’re in a V.A. Health plan, did you know that there are plans available for you that can put money back into your social security check, give you access to civilian providers and give you additional benefits.

Well, you’ve met 6 clients of mine and heard their stories in these 3 podcasts. I hope that you’ve come to see that there is no one-size-fits-all plan and that a plan that meets one person’s needs does not necessarily fit for others. Each has its place. Capture this QR code or click this link to try out our Medicare calculator and select the option that might best fit you.

I’ve got a question for you: Who would you call if you had a heart pain?

• A 1-800# and trust that they would give you the right advice?

• A friend or family member? (Uncle Elmer said he took castor oil & it worked great for him!) Not so much, right?

• Are you the kind of person who would google “heart pain” and self-diagnose to self-prescribe based on what you read?

• There’s a lot of slick Advertising out there that catches your eye, tugs on your heart & makes you feel good. So, you grab the phone & call that 1-800# so they’ll send you the new miracle treatment? No, chances are high that you would call the best Cardiologist in town. So why not call a proven, local insurance agent to help you find a Medicare plan? You’d be surprised how many fail to do this and as a result often make costly mistakes that they later regret.

What sets us apart?

• We carry the major plans & stay up to date with changes throughout the year.

• We’ll help you stay with your doctors. That’s one of our highest priorities. We’re not just going to put you on a plan that will pay us a high commission.

• We’ll research your medications and find plans with your lowest premium and medication cost.

• We’ll secure a plan which meets your unique needs.

• & BTW – We Return phone calls!

Well, we’re going to wrap this up, but can I ask you a favor? If the guidance I’ve given you today was of value, hire me as your agent to help you find the right plan!

The good news? I don’t charge for my services; The insurance companies pay me when you sign up. So, employ me. I’d love to be your personal agent, your boots on the ground!

Incidentally, we also offer Affordable Care Act plans for those under 65, and much more. So, check out our website and click on the BBB logo there to find out what others have to say about our service. Then tell your friends & family you’ve found the best agent in the whole state! Just Kidding 😊. But do send me the names of family or friends that need our help! We’ll do our best for you and for them!

I look forward to working with you in the days to come to help you find a plan that is of great value – that’s uniquely you! Thank you for your time!

This series was written by Tim Allen who has been helping Medicare beneficiaries since 2005, TX License 1355125. He is the founder of Your Retirement Inc and Sales Production Coach at Affordable Health Insurance Agency where he’s trained his agents for the past 14 years. He is a Certified Senior Advisor, a member of both the Multi-Million Dollar Round Table and the National Association of Insurance and Financial Advisors. His bride has stuck with him for 45 years and they’ve been blessed with 2 wonderful children, 6 grandchildren, and one “in the oven.” Favorite pastimes include performing, composing & arranging music, kayaking, fishing, woodworking and being a Papa to his grandies.

This podcast is his original work and the pictures within are his exclusively or he has purchased the right to use them.

Credits: